HUD is the reason this new $135,000 distinction ($800,000 minus $665,000) to your contrary home loan company, according to Sather

February 7, 2025 7:02 pm Leave your thoughtsLast week-end my teens companion died within 62. Partly due to illness, the guy turned into financially confronted later in life.

Their family guarantee could have been lay to help you an effective explore. First bills, defectively needed domestic repairs, and you may sometimes, an enjoyable food away.

My personal companion is from his very own notice. Somehow, somehow, he previously an emotional take off in the tapping into their household guarantee. Or, possibly he had been fine as he is.

Over the years, You will find obtained some phone calls out-of stressed older people. But don’t-the-quicker, they are fortunate of them with that motherlode out of possessions – a property. Many remember downsizing. That tends to be unsavory, really state.

All senior’s problem is different. You’ll find three essential situations you ought to consider just before thinking about the potential for breaking down domestic security.

Earliest, loan providers usually do not deny your home financing or discriminate facing your as the of your own age. No matter whether youre 90 yrs old and you are taking out, say, another 30-season home loan. For people who perish through to the home loan is reduced (because you failed to some alive up until many years 120), the heirs can be assume current mortgage.

Next, before going to help you a financial counselor, home loan people or even a realtor, get the person you believe probably the most in daily life to give your nonjudgmental emotional support. Never feel embarrassed or ashamed. The older you earn, the easier its to-be cheated, stressed and you can influenced of the a salesperson. You want anyone is likely to corner whom has no a good canine about endeavor.

Also, have you got other assets you might tap in addition to family security? Are you experiencing parents, siblings, pupils otherwise anyone else that will financially aid you? Therefore, let them thought working for you.

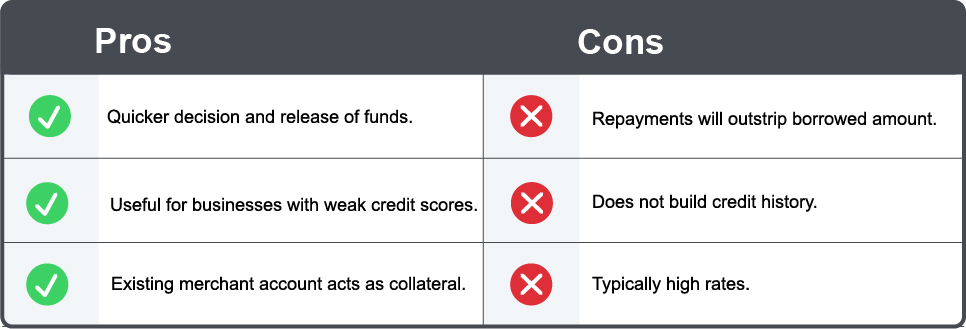

Even the extremely contemplated mortgage system to have older people (decades 62 and over) ‘s the HECM or family collateral sales financial, and the so-titled contrary financial.

The top idea is going to be in a position to utilize your domestic guarantee without the need to ever build an alternate house commission. You could stay static in our house until you perish.

You, nor their heirs, cannot are obligated to pay more than you reside really worth, regardless of how a lot of time you live, claims Joey Sather, a mortgage loan creator on Mutual away from Omaha Contrary Financial.

Note: Your own heirs features up to 12 months just after your dying so you can pay back the reverse financial (always of the offering the property). When your adversely amortizing financial collected to express $800,000 (since you long outlived the latest actuary desk anticipate) although family offered having $700,000, their home manage owe the loan bank 95% of the $700,000 value of otherwise $665,000.

The fresh drawback out of a reverse financial so is this most recent rising attention rates ecosystem performs up against you as the HUD spends predictive acting in order to imagine yourself span and you may restriction loan amount.

Reverse mortgage loans is actually negatively amortized according to the funded loan amount. The greater the fresh note price, quicker the loan equilibrium builds, and you can less funds appear.

A beneficial 75-year-old you will extract around 56.8% of their residence’s really worth considering an expected six.245% interest (since )pare by using fifty.1% out-of potential collateral pullout to the an effective 4.875% speed (since ). Incase a value of regarding $700,000, you’d be considering a max amount borrowed off $350,700 compared with a maximum out-of $397,600 if asked rates is dramatically reduced at cuatro.875%.

In addition there are an equity range-of-borrowing from the bank component within a variable-rate reverse financial while the remainder unused credit line grows big – for your benefit – in the foreseeable future.

Fog-the-mirror may be good solution, otherwise a much better alternatives versus an opposing financial. Providing you enjoys a good credit score there aren’t any other qualifying words. Work and you can earnings areas of the loan app remain empty. You might cash-out doing 70%, accepting possessions philosophy doing $5 mil. Our company is talking mortgage amounts as much as $step 3.5 billion.

The fresh FHA reverse financial understands assets viewpoints up to $step one,089,3 hundred and never a cent more, no matter the true home really worth is.

New drawbacks could you be enjoys a payment additionally the bucks-away rate are 9% to help you 9.25% into a 30-season fixed. You can use the dollars-away and place it toward a high payment Video game, state during the cuatro% in order to 5% to offset some of the foggier interest expenditures.

The least expensive amortizing mortgage may likely getting a conventional Fannie Mae otherwise Freddie Mac 30-seasons fixed speed, cash-aside financial. Today, you are looking at a speed of about six.5% for money-aside. Youre acceptance to 80% (of the home value) so you’re able to cash out. You do have so you’re able to qualify.

One particular fascinating, least-identified home loan are a member of family of your own Fannie financial, and it is called a grandfather financing. It is to have people trying to promote casing because of their parents. If the father or mother otherwise moms and dads can’t performs or manage n’t have sufficient income so you can be eligible for a home loan on their very own, the baby is the holder/tenant. The same regulations use. Cash-out over 80% loan-to-worth.

Most other prominent says are attention-just mortgages, mainly house collateral lines of credit. You could potentially always have them without having any costs related. You’ll be able to shell out attention-only, but visitors be mindful, the fresh pricing bring.

The prime speed is eight.75%, and it is gonna see 8.25% a few weeks following the Federal Set-aside brings up rates. Almost every HELOC was pegged with the prime price. Which is a beneficial product when you have a minimal first home loan you won’t want to touch.

While you are earlier, in need of assistance and now have home security, there are many means you are able to get truth be told there. You has worked the complete lives to accumulate financial assets. Faucet your house equity if necessary. You simply can’t carry it to you.

Freddie Mac computer rate information

The fresh 29-seasons fixed rate averaged 6.73%, 8 foundation situations more than the other day. The fresh fifteen-seasons repaired rates averaged 5.95%, 6 foundation circumstances more than last week.

Associated Posts

Conclusion: Assuming a borrower gets the average 29-year repaired price on a compliant $726,2 hundred financing, history year’s payment are $1,295 lower than which week’s fee of $cuatro,700.

Everything i get a hold of: In your area, well-licensed individuals can get next repaired-rate mortgages with one point: A 30-year FHA during the six%, an effective fifteen-12 months old-fashioned in the 5.875%, a thirty-season conventional from the 6.375%, a 15-seasons antique higher harmony at six.375% ($726,201 so you can $step one,089,300), a thirty-seasons large harmony traditional during the six.99% and a great jumbo 29-12 months fixed in the 6.625%.

Note: The fresh 30-seasons FHA compliant loan is limited so you can fund away from $644,000 regarding the Inland Empire and you will $726,two hundred into the Los angeles and you will Lime areas.

Categorised in: where can i have cash advance?

This post was written by vladeta