Lenders dominating financial markets and infuriating banking institutions

October 20, 2024 4:33 pm Leave your thoughtsFlower and https://www.cashadvancecompass.com/installment-loans-ks/wichita you can Paul continue to be settling in to their new house. They, such as about three-household away from Australians, put a brokerage to prepare the loan. ( ABC Development: Scott Jewell )

Whenever Flower try swinging from local Victoria to help you Melbourne’s leafy outskirts, she was not attending head into a lender part so you can type out the financing.

“I find that by going right through an agent, it is a lot more of a sleek provider, it is a lot more customised towards the demands,” she states.

Just 5 years in the past, lenders blogged 55 per cent of all the lenders into the Australian continent. Soon that can top 75 %.

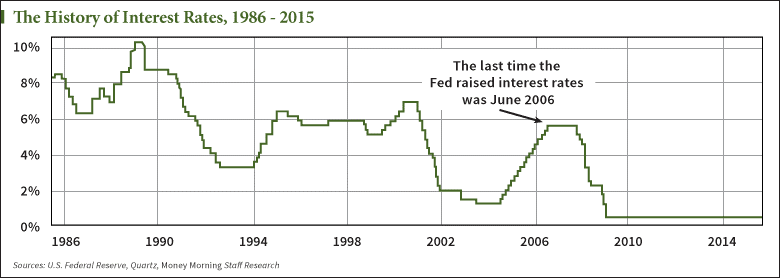

The day through to the Set-aside Bank’s most recent panel appointment to put interest levels, agents say they are busier than before.

Its business continues to grow even after agents nevertheless are paid-in an easy method a royal percentage features described as “conflicted” and “currency to possess little”.

Representative increase

2 yrs out-of high hikes inside interest levels provides sent significantly more consumers in order to brokers to get a far greater contract to their home financing and reduce devastating repayments.

“After you reach a brokerage, i make you several options, and agents essentially pick the finest rate online in the the marketplace.”

The fresh studies off peak muscles the loan & Finance Relationship out of Australia (MFAA) located to your quarter in order to Summer lenders composed 73.7 per cent of all brand new home fund, next-high effect to your listing and a good 6.5 commission part raise on same one-fourth just last year.

Billions from inside the play

If you want to know as to why banks are unhappy into development of agents, a round shape can assist: $100 mil.

“It isn’t really just towards the helping all of them have the home loan, but educating all of them around what is required, having them ‘finance ready’, permitting them understand the landscaping complete,” she states.

This new strength – and development – try quite a distance as to the appeared as if taking place to your business inside 2018, whether it was savaged to own an excellent raft from problems and you will scams which were dudding people.

Payment kicking

Commissioner Kenneth Hayne named they “conflicted remuneration” and you will derided trailing money, lasting consistently beyond when finance was indeed create, as “currency for nothing”.

Administrator Kenneth Hayne told you it actually was “quite difficult to decide to have whom a large financial company serves”. ( AAP: David Geraghty )

At the time, an abundance of loans appeared via brokers. Nonetheless it try a lower percentage of all round markets.

Around forty per cent of the many Commonwealth Bank loans emerged through agents if the royal fee is exploring the material. For ANZ it was 55 percent.

Mr Hayne knew the necessity of brokers permitting borrowers with information about what was likely “by far the most rewarding resource they will certainly pick in one deal”.

“The lender pays the fresh broker, maybe not the new borrower. Typically, the lender will pay a payment, both a right up-top fee and a path commission … The lending company seeks to alleviate the latest agent as the agent, and have the broker treat it as broker’s common bank. Yet, at the same time, the financial institution will bring within the deals that have agents and you can home loan aggregators that they act on the borrower, maybe not the lender.”

This new payment was also disturbed by evidence one to in some cases brokers “did not generate sufficient inquiries, or failed to find sufficient confirmation” from borrowers’ financial things.

“The reality that the brand new agent is actually paid as long as financing application functions really stands because a glaring purpose for that particular run,” the fresh declaration read.

“Its regarding broker’s economic appeal to get the lender agree the mortgage … costs by the banks to help you intermediaries has created certain to take part in other types out of shady perform.”

Categorised in: my payday loans

This post was written by vladeta